- Milk Road Macro

- Posts

- 🥛 Is the business cycle accelerating? ⏩

🥛 Is the business cycle accelerating? ⏩

This is one of the most important things to watch.

Tomas

July 17, 2025

GM. This is Milk Road Macro, the newsletter that spots economic turns quicker than you can say “Fed meeting recap”.

Here’s what we got for you today:

✍️ Is the business cycle about to power up markets?

🎙️ The Milk Road Show: Why This New Macro Cycle Will Break the Fed's Playbook w/ Jim Bianco

🍪 Trump plans tariff letters to 150+ countries at 10 or 15%

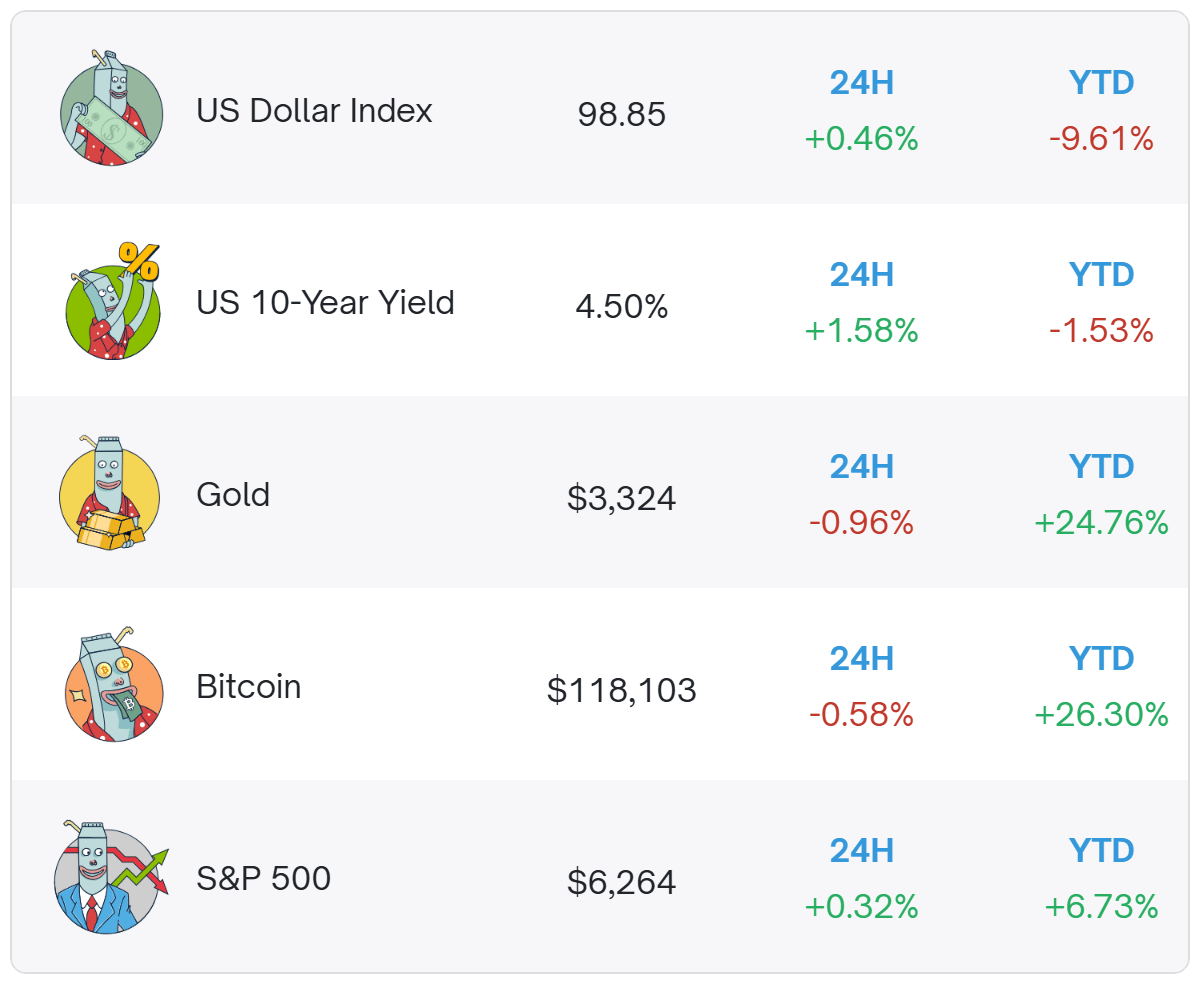

Prices as of 8:00 AM ET.

IS THE BUSINESS CYCLE ABOUT TO POWER UP MARKETS?

The business cycle could be accelerating.

This is important from an investing standpoint.

It’s more important than Trump, more important than tariffs, more important than the Fed and more important than Middle East conflicts.

So what is the business cycle and why is it important?

What are the charts telling us in terms of where the business cycle is heading next?

What are the fundamental reasons behind a potential business cycle upturn?

And of course, what does this mean for markets?

Let’s take a look…

What is the business cycle and why is it important to investors?

The business cycle is the repeated pattern of economic ups and downs that affects asset prices.

There are many ways to measure the business cycle - but for this newsletter, let's use the ISM Manufacturing PMI (Purchasing Managers Index) as our “anchor”.

The PMI provides insights into the strength of the American manufacturing sector, which is the most cyclical part of the economy.

PMI above 50 (expansion) = increased demand for goods and services.

PMI below 50 (contraction) = decreased demand for goods and services.

What has been unusual about recent years is that the PMI has remained stubbornly low, largely below 50, but generally grinding higher.

But there are now signs across global markets that the PMI could be heading for a “real” expansion phase.

This would mean higher growth, higher corporate earnings and higher investor confidence.

When the PMI is strongly rising, asset prices as a whole almost always rise.

And, in particular, we historically see capital “moving out along the risk curve”, and finding a home in more speculative assets, as confidence grows.

This is why we have historically seen all bitcoin and crypto “mania phases” coinciding with a strongly rising PMI.

So, let’s run through a lot of charts that are currently showing a positive outlook for the business cycle.

Chart bonanza

The one thing I have found that is the most correlated to the PMI in recent years is ARK Innovation ETF.

This is a US equity fund focusing purely on “disruptive innovation”.

ARK is a good indication of the more speculative end of the US stock market.

It’s remarkable how closely this has tracked with the PMI in recent years, with a roughly two month lead.

It’s currently signaling PMI at around 54 by August/September.

This rising speculation is also evident when looking at “high beta” stocks relative to the S&P 500 (SPHB/SPX).

High beta is currently outperforming the S&P 500 at the fastest rate since the previous business cycle upturn (2020/2021).

This measure didn’t really start to turn up throughout 2024, but now it’s bouncing strongly, giving me more confidence that we may be entering “the real turn” in the business cycle.

I looked in detail at the copper/gold ratio here - it is a very important indicator of where we are in the economic cycle.

It now looks like it could be starting to turn.

China is heavily linked to the copper/gold ratio.

China is incredibly important to the global economy - it’s the “manufacturing engine of the world”.

I believe one of the reasons why this PMI cycle has been so sluggish is that the Chinese economy was nosediving in 2023 and 2024, acting like a heavy weight on the global economy.

We can use the Chinese Government 10-year bond yield (CN10Y) as a rough proxy for the relative strength of the Chinese economy.

CN10Y was sliding into the abyss in 2023 and 2024, but since early 2025 it has stabilized and started curling upwards (CN10Y shown here as YoY percentage change).

Here’s another one from China - Chinese Credit Impulse.

This tracks the change in the amount of new credit being issued in China - measuring how quickly credit is growing or shrinking in relation to the overall economy.

It’s currently rising.

This one has some leading characteristics historically, so I’ve shifted it forward by four months.

Germany is another manufacturing powerhouse, and its economy is also heavily linked to China.

So what’s going on with economic sentiment in Germany?

It’s moving higher.

The total amount of M2 money supply in the world (denominated in US dollars) is growing at a relatively fast pace.

This generally leads the PMI by several months.

The Baltic Dry Index tracks the cost of shipping raw commodities across the world.

As manufacturing activity increases, more commodities need to be shipped.

The Baltic Dry Index is rising.

What about the dollar?

A lower dollar (vs other currencies) is good news for everyone.

It’s good for US companies, making exports more attractive, and it's good for the rest of the world, making dollar-denominated debt (the majority of global debt) more affordable.

The Trade-weighted Dollar Index is rapidly moving lower (higher when inverted).

Let’s now switch back to the US.

As the business cycle picks up, financial conditions will generally loosen.

And the Chicago Fed’s National Financial Conditions Index is falling (financial conditions loosening).

What about high yield bonds?

This can be thought of as the speculative end of the bond market.

Moving higher.

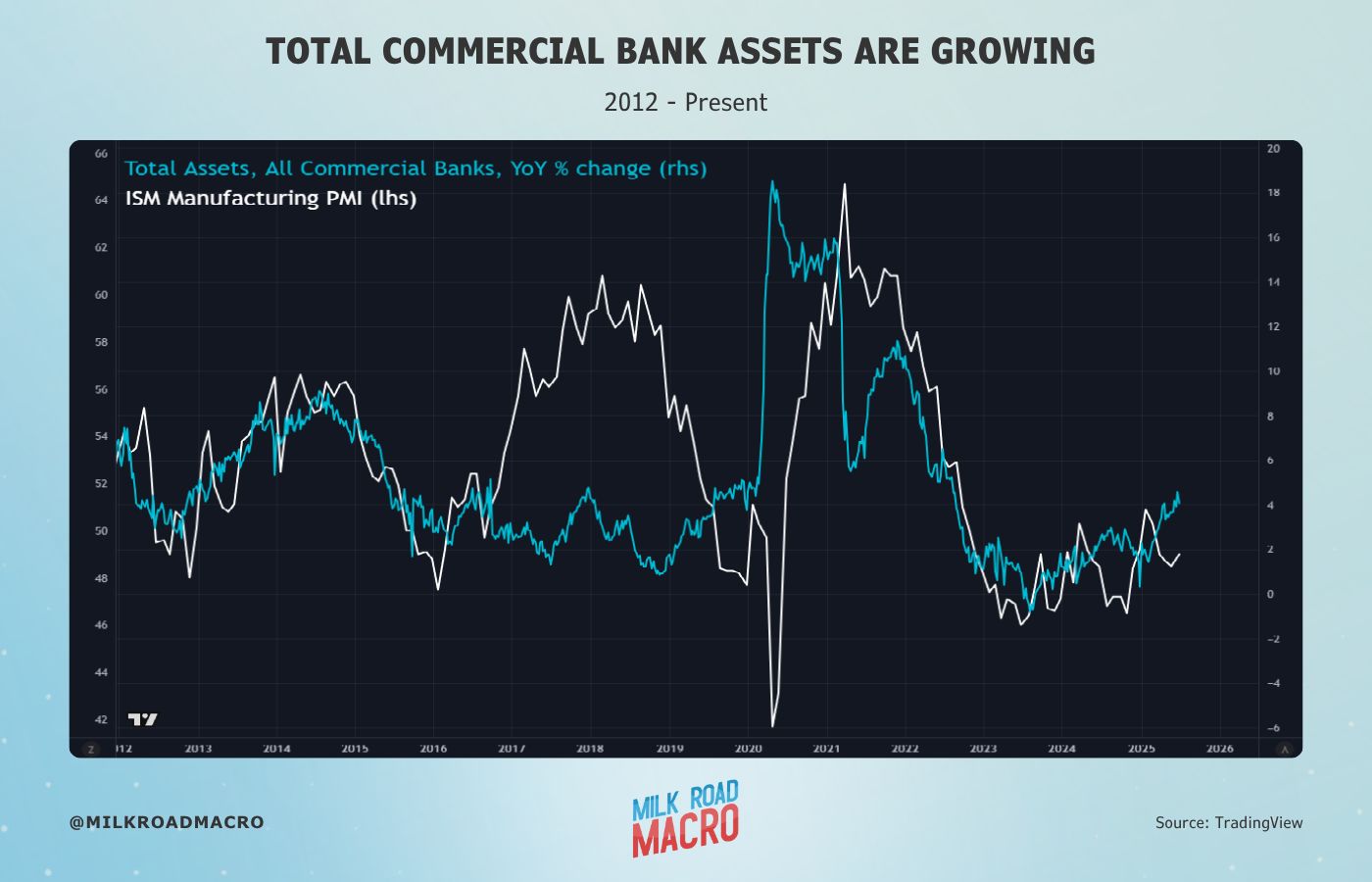

What about the size of all assets owned by US commercial banks?

Moving higher.

What about regional bank stocks?

This is a very cyclical part of the economy.

Moving higher.

So, what are the fundamental reasons for an upturn in the business cycle?

We’ve looked at the charts.

Let’s now consider the fundamental reasons why the business cycle could pick up from here.

1/ AI boom

Nearly $7 trillion in capital outlays is needed by 2030 to power the AI/digital revolution.

A McKinsey research report states:

“Data centers equipped to handle AI processing loads are projected to require $5.2 trillion in capital expenditures, while those powering traditional IT applications are projected to require $1.5 trillion in capital expenditures”

The AI boom is already accelerating and massively impacting GDP - with purchases of computer equipment adding a full percentage point to US GDP in Q1 2025 - larger than at any time during the Dot Com bubble.

2/ Trump’s “One Big Beautiful Bill”

Trump’s newly signed bill piles on more Government spending and is likely to widen the deficit to GDP, which should stimulate the economy.

Specifically within the bill is a “permanent 100% bonus depreciation provision”.

This measure allows companies to immediately deduct the full cost of a range of assets - such as machinery, equipment, and certain real property.

It’s expected to stimulate capital investment across various industries, including manufacturing, aerospace, and real estate.

The US Government is also deregulating nuclear power, largely due to AI needs - aiming to increase nuclear power generation by 300%.

This is estimated to unlock more than $2 trillion in capital spending.

3/ EU defence spending

Trump has also lit a fire under Europe to increase defence spending.

And this is happening - with just Germany alone expected to spend €649 billion over the next five years.

A recent report from S&P Global Market Intelligence details how the defence spending plans have led to the biggest jump in economic optimism among German businesses since early 2022.

German businesses are also boosting investments for the first time in two years, according to the report.

4/ China ramping up economic support

China has also been stepping up fiscal and monetary support since the start of the year.

The PBoC (the central bank of China) made the rare step in officially changing its monetary policy stance from “prudent” to “moderately loose” in December 2024.

Since then, it has injected more than $1 trillion into the Chinese economy.

Recent reports also indicate China is set to “ramp up and broaden fiscal support” in the second half of 2025.

Wrapping up

The business cycle as measured by the PMI has been sluggish, to say the least, over recent years.

My opinion is that a lot of this may be due to a faltering Chinese economy weighing on the global economy.

But there are signs that China is now waking up - alongside Europe.

And the US will also likely see stimulative effects from Trump’s new bill and an ongoing massive AI capex spend.

It looks like it’s very possible we might be entering “the real turn” in the business cycle.

And yes, this generally means good things for risk assets like stocks and bitcoin.

And, in particular, assets further down the risk curve, like “frontier” speculative stocks in emerging industries and altcoins.

That’s it for this edition - catch you for the next one.

“THE OLD MACRO PLAYBOOK IS DEAD” 🚨

Jim Bianco just dropped one of the most reality-check heavy episodes we’ve had all year.

Here’s what you need to know:

Bianco says the 2010s are over, we’re in a new macro regime. Think remote work, deglobalization, sticky inflation, and no more zero rates.

Don’t be shocked if inflation ticks up again in H2. Tariffs are quietly juicing the CPI while used car price drops are just a mirage.

Bianco’s biggest warning: The bond market is the apex predator. If investors don’t bite at 4%, rates will just go higher, and risk assets will get crushed.

Plus: Why stablecoin rules could mean “yield-free” money markets, and why $2T stablecoins is fantasy unless Bitcoin 10x’s first.

Bottom line? Bianco says: Don’t anchor to any one macro story, and learn the bond market. Because it’s still the only thing that truly matters.

Click below to watch the full episode. 👇

Markets whipsawed yesterday amid speculation that Fed Chair Jerome Powell might be fired. Initial reports said President Trump was “likely” to fire Powell “soon” after discussing the idea with lawmakers.

Trump said he would send out more tariff letters to “more than 150 countries” notifying them of tariff rates “probably 10 or 15%”. This could be a tariff reduction for many countries, relative to the levels initially threatened.

US VC-backed companies raised $80 billion in Q1 2025, the highest venture capital investment since Q1 2022. In recent years, AI startups have attracted a growing share of VC funding.

RATE TODAY’S EDITION

What'd you think of today's edition? |

MILKY MEME 🤣

ROADIE REVIEW OF THE DAY 🥛