- Milk Road Macro

- Posts

- 🥛 Trump vs Powell: What does it mean? 🔍

🥛 Trump vs Powell: What does it mean? 🔍

This showdown could have big implications for markets

Tomas

July 15, 2025

GM. This is Milk Road Macro, your twice-a-week market briefing that’s as intense as a staredown between Trump and Powell. Popcorn not included.

Here’s what we got for you today:

✍️ Here’s why the Trump/Powell showdown is important

📊 How have you managed as capital shifts out the risk curve?

🍪 Trump warns 100% secondary tariff on Russia if no Ukraine deal

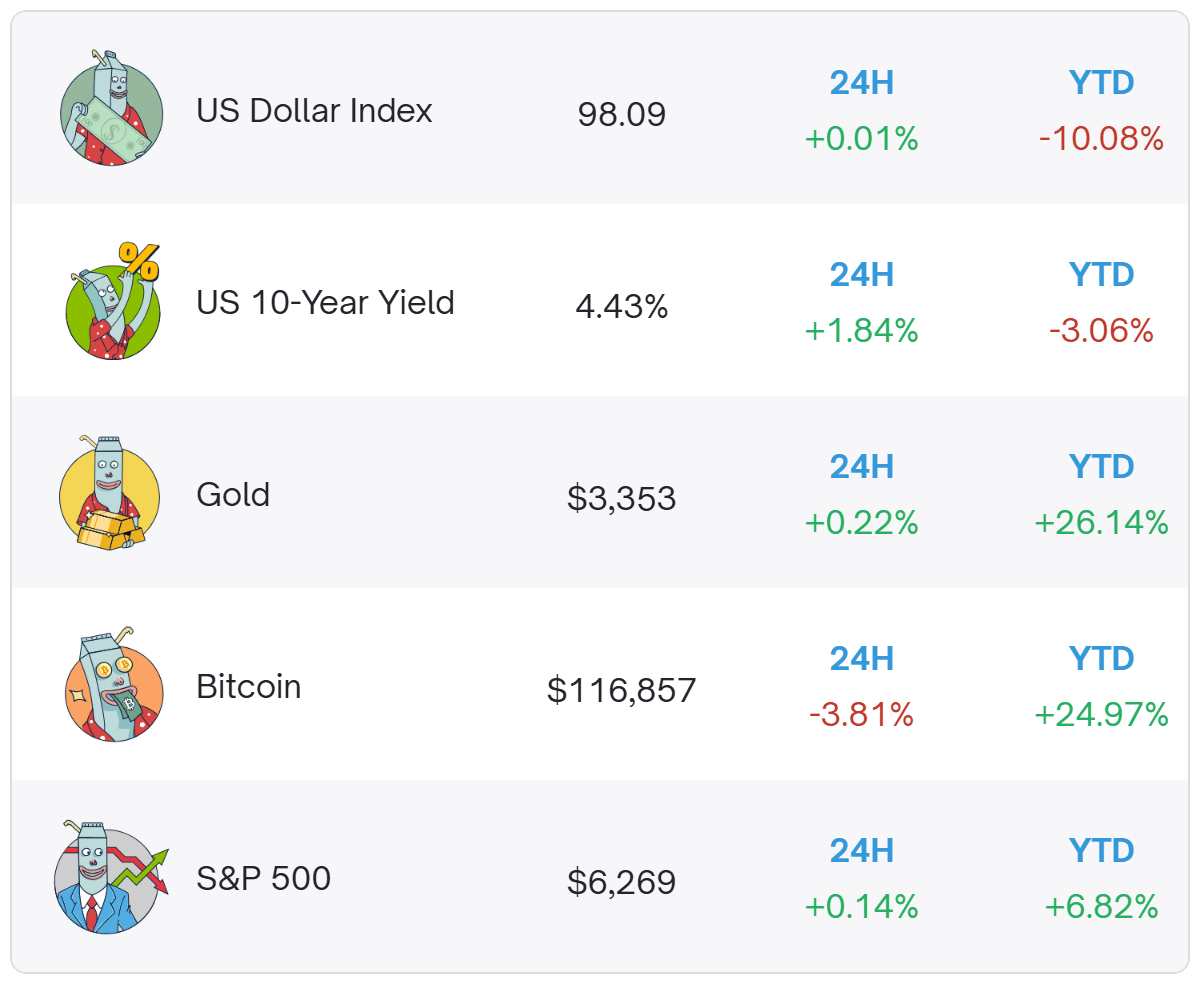

Prices as of 8:00 AM ET.

HERE’S WHY THE TRUMP/POWELL SHOWDOWN IS IMPORTANT

The showdown between President Trump and Fed Chair Jerome Powell rages on.

Trump wants interest rates lower.

And Trump wants Powell out.

But Powell is standing firm.

We know the Fed Chair is heading out the door at some point - but could he be leaving earlier than expected?

What impact will a potential “shadow Fed Chair” have?

And what does it all mean for asset markets?

Let’s take a look.

A dovish Fed Chair is coming

Trump thinks the Federal Funds rate should be a lot lower than it is now (4.25%-4.5%), maybe as low as 1%.

Trump says Powell is “stupid”, “terrible”, “a numbskull”, “a stubborn mule” and “a total and complete moron” (amongst other things).

He even sent Powell a handwritten note demanding rate cuts.

What is interesting about Trump’s stance - is that it's not so much about firing up the economy (although this is part of it) but more about reducing the Government’s debt interest costs.

Trump thinks Powell “has cost the USA a fortune”.

On Truth Social, the President wrote that the Federal Funds rate was “at least 3 points too high” and that it is costing the US $360bn in interest payments per percentage point on the Fed Funds rate.

Donald Kohn, former Fed vice chair, said: “That’s worrying, because keying monetary policy to relieve budget pressure is a sure track towards higher inflation”.

This is all very important, because Powell’s tenure as Fed Chair ends in May 2026, and it will be Trump who ultimately appoints a successor.

Trump has made it clear his pick “will lower rates”.

He said: “If I think someone is going to keep rates where they are, I’m not going to put them in”.

Enter: the “shadow Fed Chair”

There have been a number of reports suggesting that Trump could name a successor to Powell well before May 2026.

Reports indicate the next Fed Chair could be announced as early as September this year.

This is interesting - because it brings into play the idea of a “shadow Fed Chair”.

The market is forward-looking - it pays attention to what the Fed Chair is guiding towards, and will price that direction in.

So later this year, if the market knows who the next Fed Chair is, and that Fed Chair goes around making very dovish statements, it’s very possible the market will begin to just ignore Powell and price in the new interest rate path as sketched out by the new Fed Chair.

Essentially, the new Chair might have control of monetary policy before taking office.

But could Powell be fired early?

Things got even more interesting late last week.

The director of the Office of Management and Budget Russ Vought laid out accusations against Powell, including lying to Congress and mismanaging the renovation of the Fed (Eccles) building.

Vought says the renovation - which includes rooftop gardens, VIP elevators and premium marble - is $700 million over its initial cost and has a price per square foot of $1,923.

Vought believes some Powell comments regarding the renovation at a recent testimony need investigating.

Trump said Powell should “resign immediately” if the allegations prove true.

Some people believe the Trump administration might be building a case to meet the legal requirements needed to fire Powell before his term ends.

Asked whether Trump has the authority to fire the Fed Chair, Kevin Hassett, director of the National Economic Council, said: "That's a thing that's being looked into. But certainly, if there's cause, he does".

So, what does this all mean for markets?

The market is currently pricing in 2 rate cuts in 2025, with the first likely to come in September.

In recent weeks, there are clear signs that capital is “moving out along the risk curve”.

Looking across global markets, my general read is that the forward growth picture looks relatively decent, the business cycle appears to be ticking up, a recession is nowhere to be seen, and the biggest risk appears to be inflation rising moderately.

This is not a typical “let’s start cutting rates again” environment.

We are seeing “high beta” stocks ripping higher relative to the S&P 500 - the largest such outperformance since 2020/2021.

Below is SPHB (S&P 500 High Beta ETF) relative to the S&P 500.

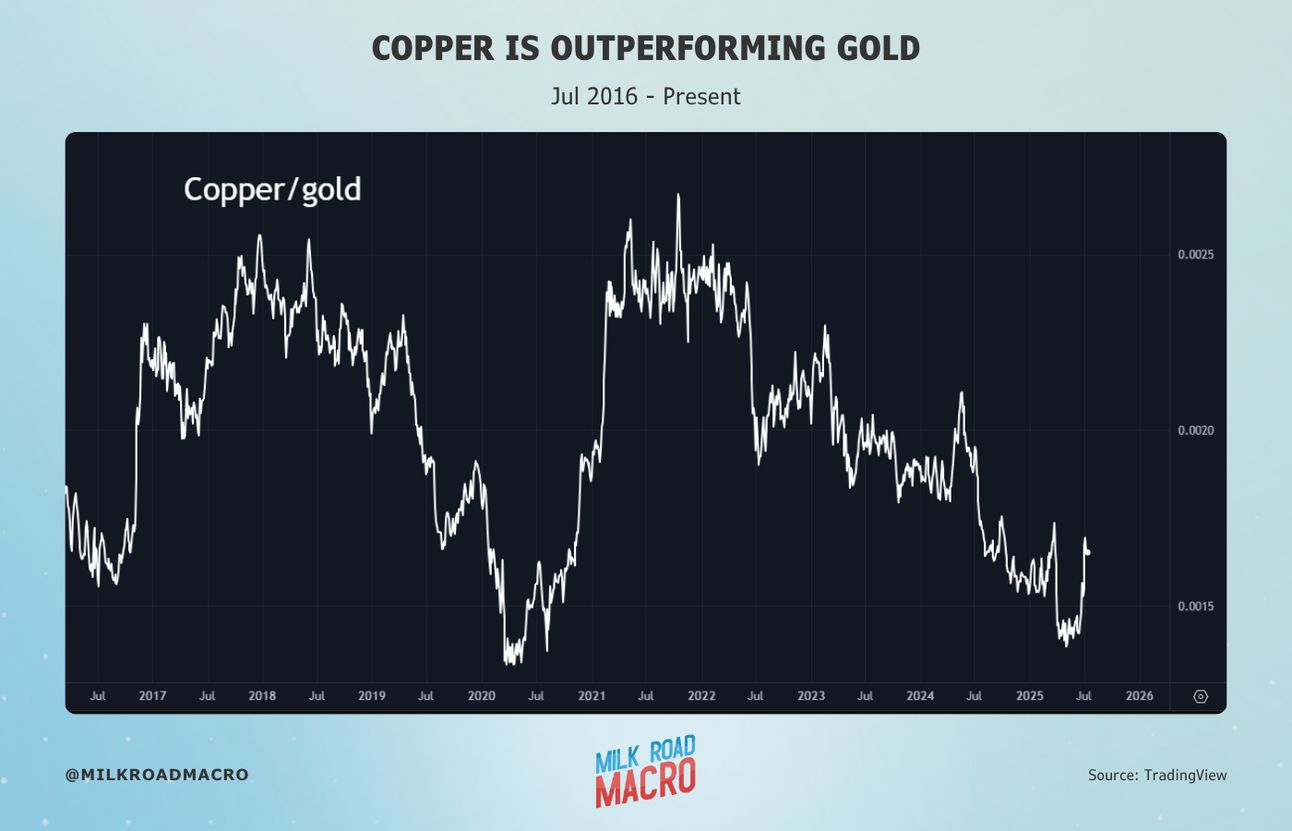

The copper/gold ratio is also ripping higher (I looked in detail at the copper/gold ratio here) - a sign of a strengthening global economy.

Bitcoin is surging to new all-time highs.

If this environment persists and the Fed starts cutting and signalling more cuts, it would likely just fuel further speculation and risk-taking, in my opinion.

Remember, we already have fiscal stimulus ahead from Trump’s front-loaded deficit widening “One Big Beautiful Bill”.

Adding monetary stimulus on top of that will likely further fuel the fire.

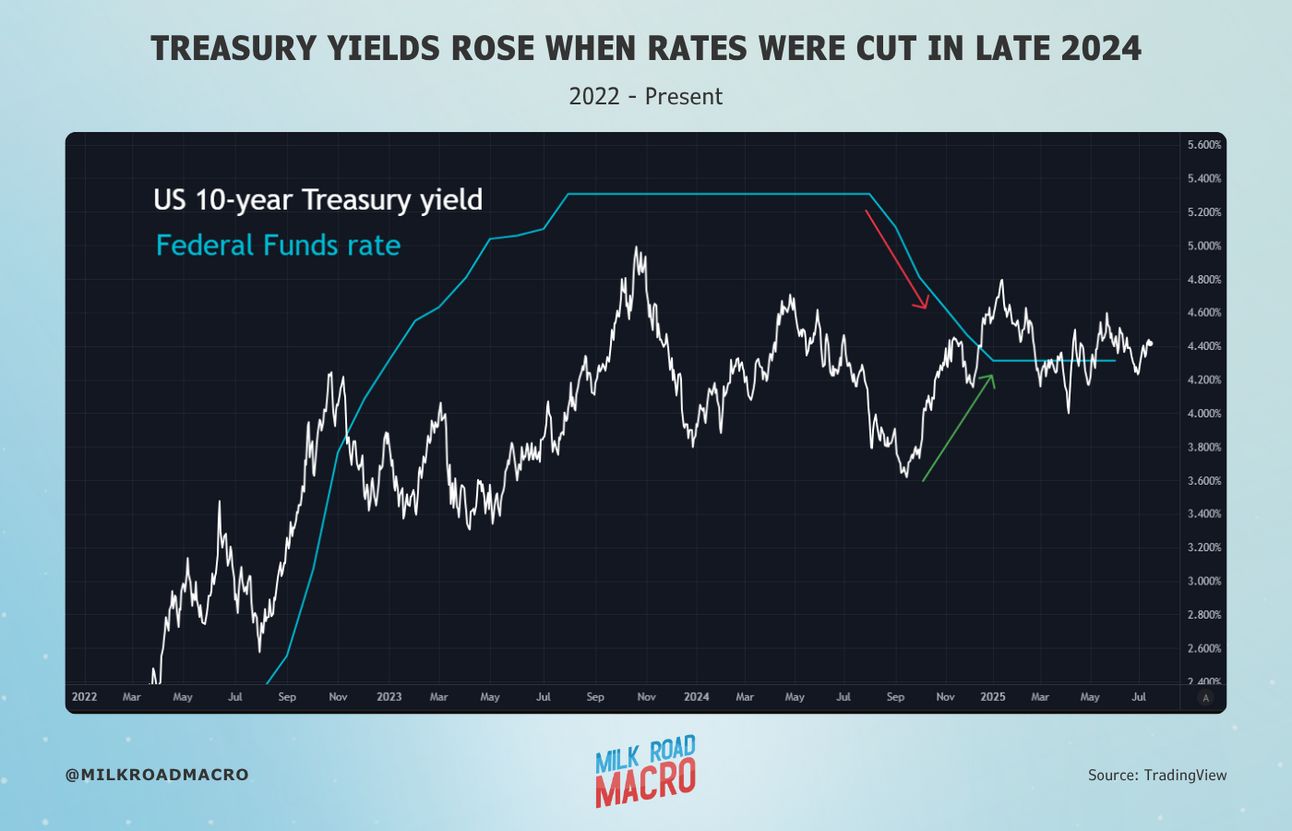

But the picture is probably not so rosy for the bond market.

Decent growth and moderately rising inflation would likely put upward pressure on long-end Treasury yields.

If the Fed were to lower interest rates, Trump’s expectation is that the entire yield curve would decline, saving the US government “hundreds of billions of dollars”.

But bond yields might not necessarily follow short-term interest rates downward.

Last year, between September and December, the Fed cut the Federal Funds rate by 100bps and the 10-year Treasury bond yield (and mortgage rates) rose by 100bps.

The “Bond Vigilantes” (correctly) recognized that the economy wasn’t as weak as Fed officials thought at the time.

I think there’s a good chance we see a re-run of late 2024 in the second half of this year (good environment for risk assets, bad environment for bonds).

And what about if Powell is dismissed early?

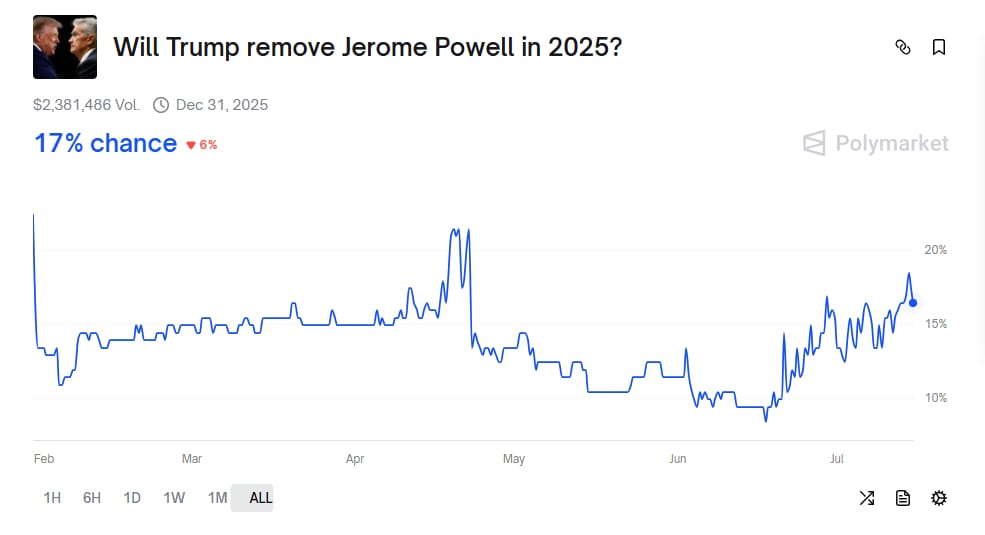

According to Deutsche Bank’s head of FX strategy George Saravelos, it’s a major potential event and an underpriced one.

The odds that Trump removes Powell in 2025 on Polymarket currently sit at 17%.

Saravelos believes a Powell firing could trigger a rapid sell-off in both the dollar and US Treasuries.

If Trump were to force Powell out, the subsequent 24 hours would probably see a drop of at least 3% to 4% in the trade-weighted dollar, as well as a 30 to 40 basis-point fixed-income selloff, Saravelos said.

He added: “Investors would likely interpret such an event as a direct affront to Fed independence, putting the central bank under extreme institutional duress”.

Wrapping up

Powell is going - and a new, more dovish Fed Chair is coming.

This is now very apparent.

But questions remain over how long Powell can cling on for, and whether or not he might be “overshadowed” by his successor anyway even if he remains.

In my opinion, rate cuts in the current market environment would further feed the rising risk-taking sentiment.

But they may well push Treasury yields higher - the exact opposite outcome to what Trump is yearning for.

That’s it for this edition - catch you for the next one.

POLL OF THE WEEK 📊

Last week, we asked you:

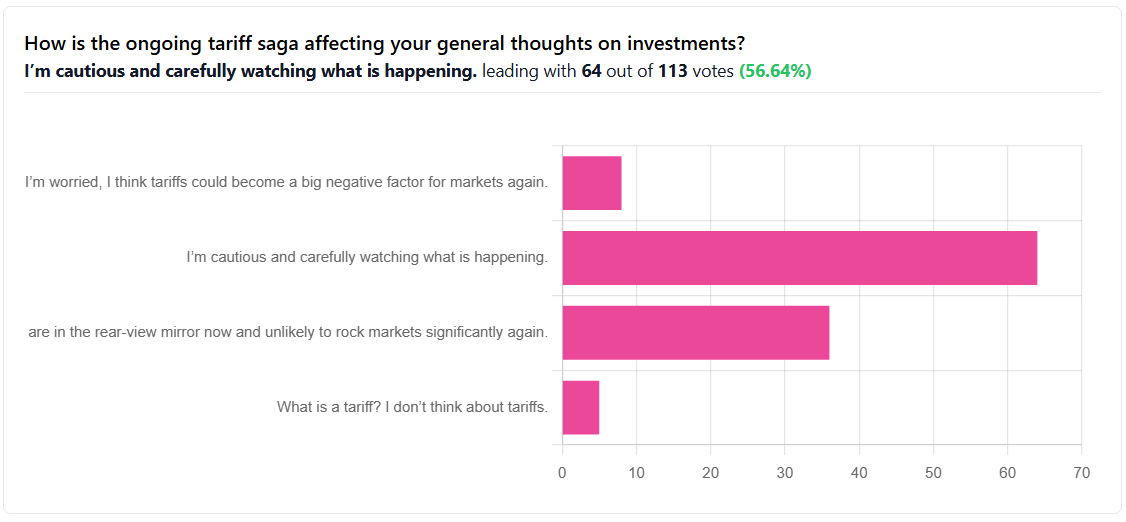

How is the ongoing tariff saga affecting your general thoughts on investments?

More than half of respondents said they were “cautious and carefully watching what is happening”.

While around 30% believed tariffs were in the rearview mirror and unlikely to rock markets again.

This week, we are asking you:

Since early April, there are clear market signs that capital is “shifting out across the risk curve” - but how have you managed your investments? |

President Trump has threatened Russia with a “100% secondary tariff” if a Ukraine peace deal is not reached within 50 days. He also announced more US weapons will be available to Ukraine.

Nvidia plans to resume sales of chips to China, after previously being restricted. Chinese companies have scrambled to place orders for the chips.

Meta’s CEO Mark Zuckerberg said he is focused on building mega AI data centers - and the first one is called “Prometheus”. The efforts are part of massive and unprecedented capex plans among big tech firms that could surpass $1 trillion by 2027.

RATE TODAY’S EDITION

What'd you think of today's edition? |

MILKY MEME 🤣

ROADIE REVIEW OF THE DAY 🥛