- Milk Road Macro

- Posts

- 🥛 When will the Fed cut rates? ✂️

🥛 When will the Fed cut rates? ✂️

Let’s run through the main points from FOMC.

Tomas

July 31, 2025

GM. This is Milk Road Macro, the newsletter that breaks down monetary policy smoother than Powell dodging a Trump tweet.

Here’s what we got for you today:

✍️ Powell holds steady, but cracks are showing

🎙️ The Milk Road Macro Show: Rate Cut Chaos: Inside the Fed’s July Meeting Standoff w/Tony Greer

🍪 Strong US earnings boosted by big tech results

Prices as of 8:00 AM ET.

POWELL HOLDS STEADY, BUT CRACKS ARE SHOWING

It’s that time again.

It’s Fed week, where the finance world gathers round to watch a man in a suit talk a lot but not really say much.

President Trump has been continuing his attacks on Fed Chair Jerome Powell in recent weeks, demanding that interest rates be slashed.

So, what happened at the FOMC meeting this week?

Are we seeing a fracturing within the Fed as economic data divides opinions?

How did markets react?

And what will happen next?

Let’s take a look…

So, what happened at the meeting?

In a surprise to nobody, interest rates were held steady by the Federal Reserve on Wednesday (markets were expecting a 98% chance of this occurring).

It was another “wait-and-see” meeting, although the Fed still clearly has a “cutting bias”.

The market had hoped that Powell might be willing to “lean dovish” and open the door a little wider towards a rate cut restart in September.

But instead, Powell’s press conference had a slightly hawkish bias.

Powell reiterated that the Fed is “well-positioned” to cut rates when needed, but dampened expectations of a September rate cut, without closing the door completely.

President Trump’s tariffs have injected uncertainty into the economic outlook and the Fed’s policy outlook.

Powell said:

“A reasonable base case is that the [tariff] effects on inflation could be short-lived, reflecting a one-time shift in the price level, but it is also possible that the inflationary effects could instead be more persistent — and that is a risk to be assessed and managed.”

He added:

“We’re still a ways away from seeing where things settle down. Yes, we are learning more and more. It doesn’t feel like we’re very close to the end of that process.”

And Powell fired a shot back at Trump, who has been demanding rate cuts primarily to ease the US Government’s soaring debt interest costs (now $1 trillion per year).

Powell said:

"We don't consider the fiscal needs of the federal government. No advanced economy central bank does that, and it wouldn't be good for us to do so as it would compromise our credibility."

It seemed odd that we didn’t get an immediate angry reaction from Trump following the press conference.

But then today, it arrived.

If you want to go deeper, we sat down with Tony Greer just after the meeting to break it all down — what the Fed’s move means for inflation, markets, and the second half of 2025.

Watch the full episode on YouTube now and make sure you’re subscribed to the Milk Road Macro channel to stay ahead of the next big shift.

A fractured Fed

In recent years, the Federal Reserve has almost always been unified in its interest rate decisions.

But not this time.

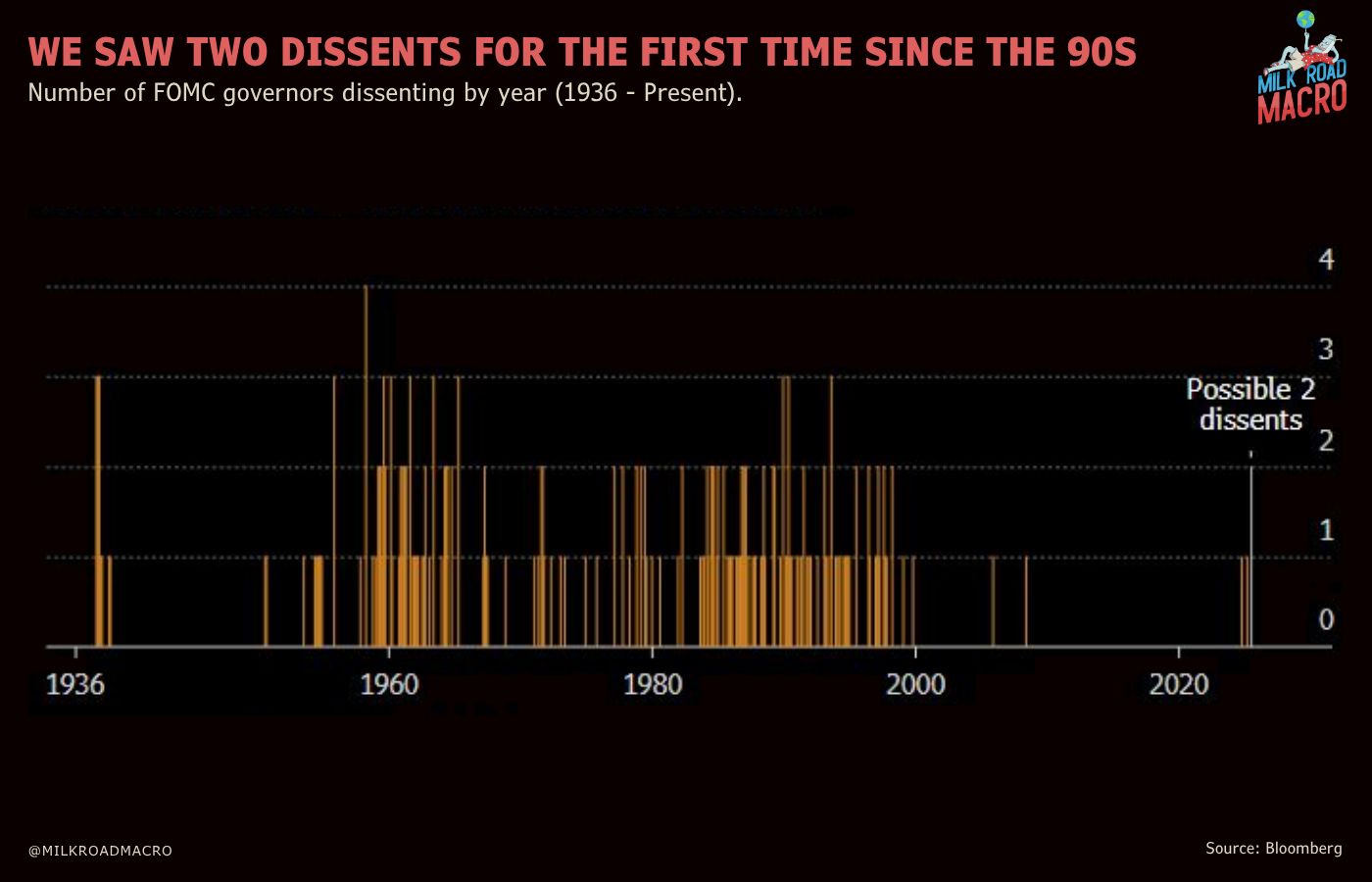

This week we saw two dissents from Governors - the first time this has happened since the 90s.

Governors Christopher Waller and Michelle Bowman both thought a rate cut was the right thing to do this week, and disagreed with the decision to hold rates steady.

Some people have argued this dovish stance is a political choice to “get in Trump’s good books” as Governors jostle for the top job, with Powell’s term as Fed Chair ending in May 2026.

JP Morgan’s chief US economist Michael Feroli joked that “two job applications were attached to the FOMC statement”.

Regardless, both Bowman and Waller laid the groundwork for their dissents before the meeting.

Bowman pointed to signs of fragility in the labor market, while Waller said slowing private-sector payrolls also signaled underlying weakness in the US employment landscape.

At the press conference, Powell said policymakers would be paying attention to downside risks in the labor market that are “certainly apparent”.

But he described the labor market as solid, and said the Fed is closer to its goal of fostering maximum employment in the economy than it is to its 2% objective for inflation.

Interestingly, according to Viraj Patel of Vanda Research, dovish Governor dissents generally lead policy moves.

He said: “There have only been 14 dovish Governor dissents since 1987. Excluding hiking cycles, the Fed has typically gone on to cut 50bps in the next 3 months".

How did markets respond?

While the Fed is still firmly in a “cutting cycle” and rate cuts are still expected this year, Powell’s slightly hawkish tone caught markets somewhat off-guard.

The dollar (as measured by the Dollar Index) rallied for the fifth straight day to its highest close in two months.

For a few weeks, we’ve been outlining the case for a reversal in the dollar, largely due to incredibly bearish positioning and sentiment.

This now looks well underway.

Major US stock indices like the S&P 500 and Nasdaq initially wobbled after the slightly hawkish FOMC press conference.

But then staged a huge comeback later in the day, reversing the earlier losses.

This was largely due to blow-out tech earnings reports later in the day, sending Meta (+10%) and Microsoft (+9%) soaring higher, as both beat analyst expectations.

The Russell 2000 (US small-caps) which includes smaller and more interest-rate sensitive companies, fell during the FOMC meeting and stayed down.

Bitcoin also fell during the press conference but then rallied higher again, following large cap US stock indices.

So, what happens next?

Now we wait for the next FOMC meeting - which will not take place until September 16-17.

Powell’s hawkish tone yesterday caused markets to slash rate cut expectations for the September meeting.

Earlier this week, market pricing of a 25bps rate cut in September was as high as 65%.

Now, this has been cut to just 43%.

But the Fed will see a lot of new data between now and then, including two rounds of inflation prints and two rounds of unemployment/jobs data.

While it’s almost two months until the next official Fed meeting, we do also have Jackson Hole in the meantime, taking place on August 21-23.

This is the annual central bank jamboree, when global central bankers gather in Wyoming to talk about central bank stuff.

But it could be important, because the Federal Reserve does have a liking for using Jackson Hole to signal big policy pivots in front of the dramatic backdrop of the Rocky Mountains.

This has happened on two occasions in the last three years.

Powell’s famous “there will be pain” speech in 2022 rocked markets and was followed by the Fed continuing to relentlessly hike rates through the rest of that year.

And in 2024, Powell signalled a sudden and unexpected dovish pivot at Jackson Hole, which was followed by the start of the Fed’s current rate cutting cycle in September 2024.

It’s very possible that Powell could use Jackson Hole next month as his main “signalling event” and firmly signal whether or not the Fed will restart rate cuts in September.

Wrapping up

The market had been hoping for a dovish tilt, but instead it got a slightly hawkish tone.

The Fed largely still seems uncomfortable with restarting rate cuts given the uncertainty on inflation - although there’s now clear disagreement among Governors.

But, taking a wider view, not a whole lot changed this week, with the market still expecting cuts to come at some point this year.

This is the most important thing - the Fed is still firmly in a cutting cycle.

And, in fact, slow rate cutting cycles are historically much more bullish for risk assets than fast rate cutting cycles.

It’s almost two months until the next Fed interest rate decision.

But don’t discount Jackson Hole in August as a potential big event.

President Trump unleashed a flurry of tariff deals and demands ahead of an expected August 1 deadline. This included a surprise on India and a 50% tariff on copper, with US copper futures crashing 19% in minutes.

A solid US earnings season continued with big reports from tech giants. Meta is taking advantage of its lucrative advertising business and stepping up spending next year, while Microsoft is set to follow Nvidia in becoming a $4 trillion company after confirming it is among the leaders in the AI boom.

Upper-income Americans are increasingly falling behind on credit card and auto loan payments. Delinquencies from those making at least $150,000 annually have jumped almost 20%, faster than for middle and lower income borrowers.

RATE TODAY’S EDITION

What'd you think of today's edition? |

MILKY MEME 🤣

ROADIE REVIEW OF THE DAY 🥛