- Milk Road Macro

- Posts

- 🥛 The ‘tariff fog’ is slowly lifting 🌫️

🥛 The ‘tariff fog’ is slowly lifting 🌫️

So, what’s the latest with tariffs?

Tomas

July 29, 2025

GM. This is Milk Road Macro, the newsletter that cuts through tariff talk like a hot knife through overpriced imported butter.

Here’s what we got for you today:

✍️ Tariff headlines keep coming. What’s up?

🎙️ The Milk Road Macro Show: The Fed Is Wrong About AI and the Economy w/ PDS

🍪 The FOMC meeting begins today

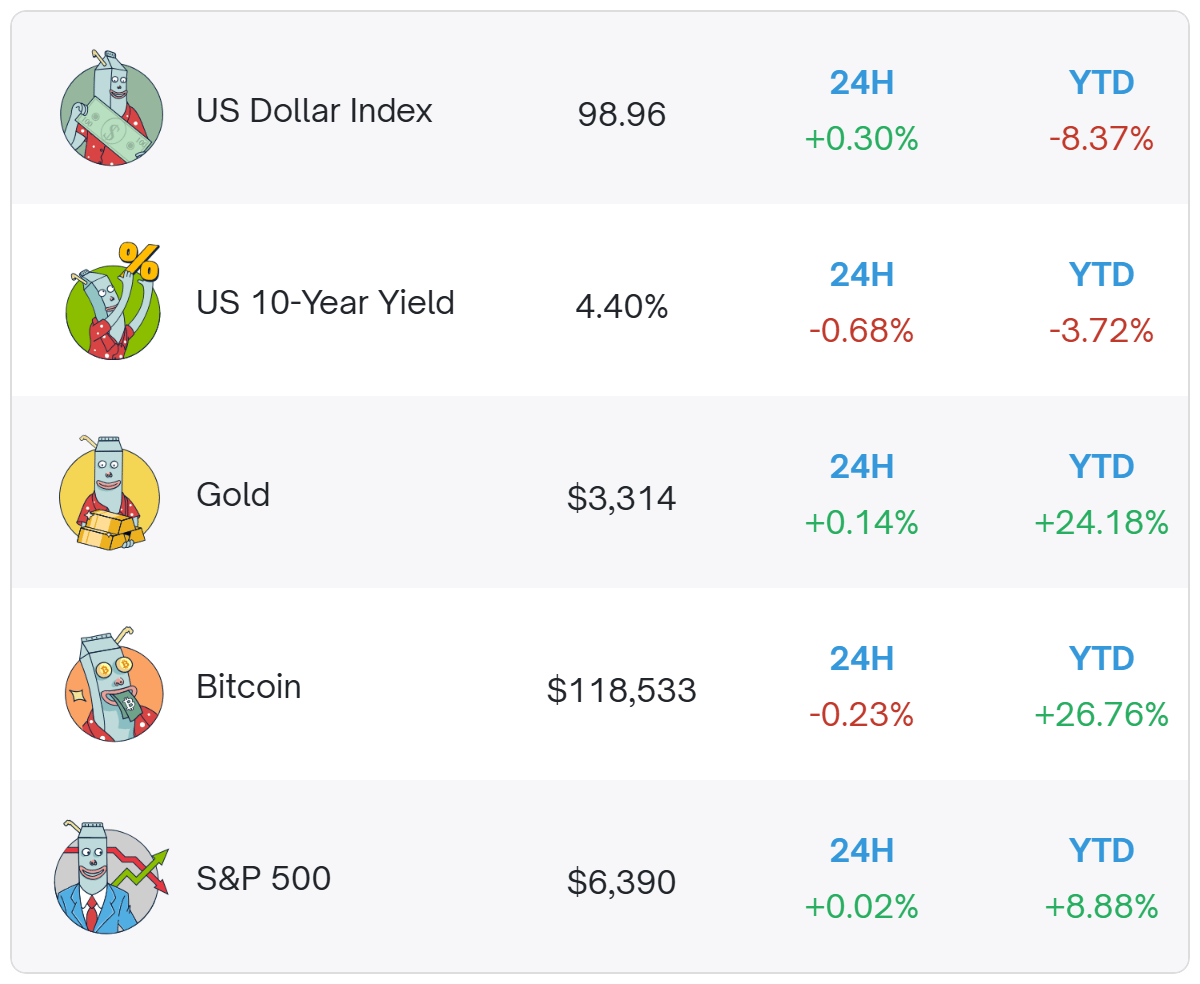

Prices as of 8:00 AM ET.

THERE’S A NEW TARIFF HEADLINE EVERY DAY - SO WHAT’S GOING ON?

Confused about the constant tariff headlines?

You won’t be the only one.

Everyday we seem to get a new soundbite.

And we still have an August 1 trade talk deadline hanging over most countries.

But deals are slowly being done - and the tariff “fog of uncertainty” appears to be lifting.

So, what’s the latest with tariffs?

And what does it all mean for asset markets?

Let’s take a look…

EU deal reached

On Sunday (July 27), a new trade deal was signed with the EU.

President Trump is pretty happy about it - but some Europeans are not so happy.

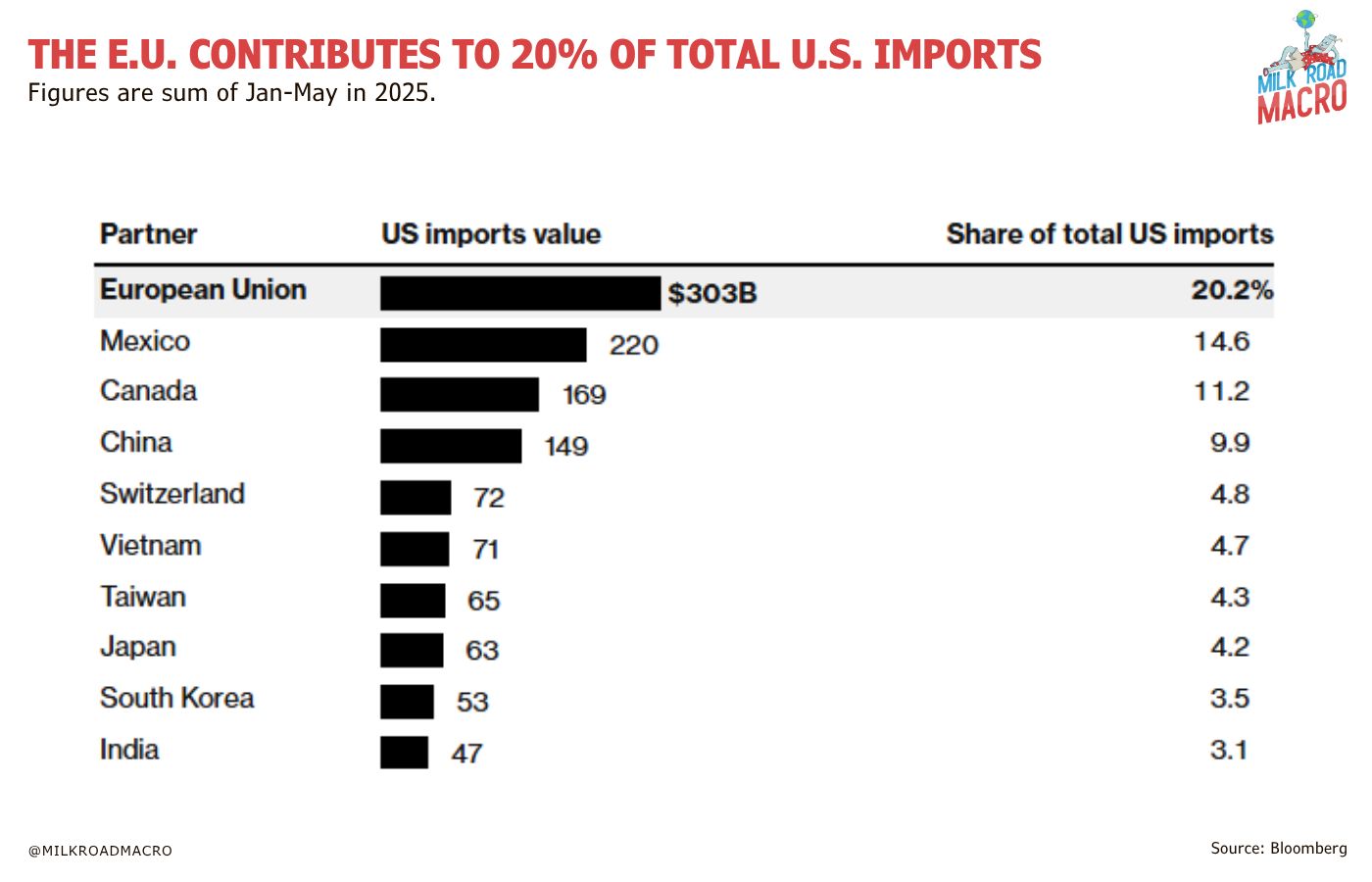

The EU is the biggest source of US imports, so this one is definitely a big one.

The EU will face 15% tariffs on most of its exports to the US, lowered from the previously threatened 30% levy.

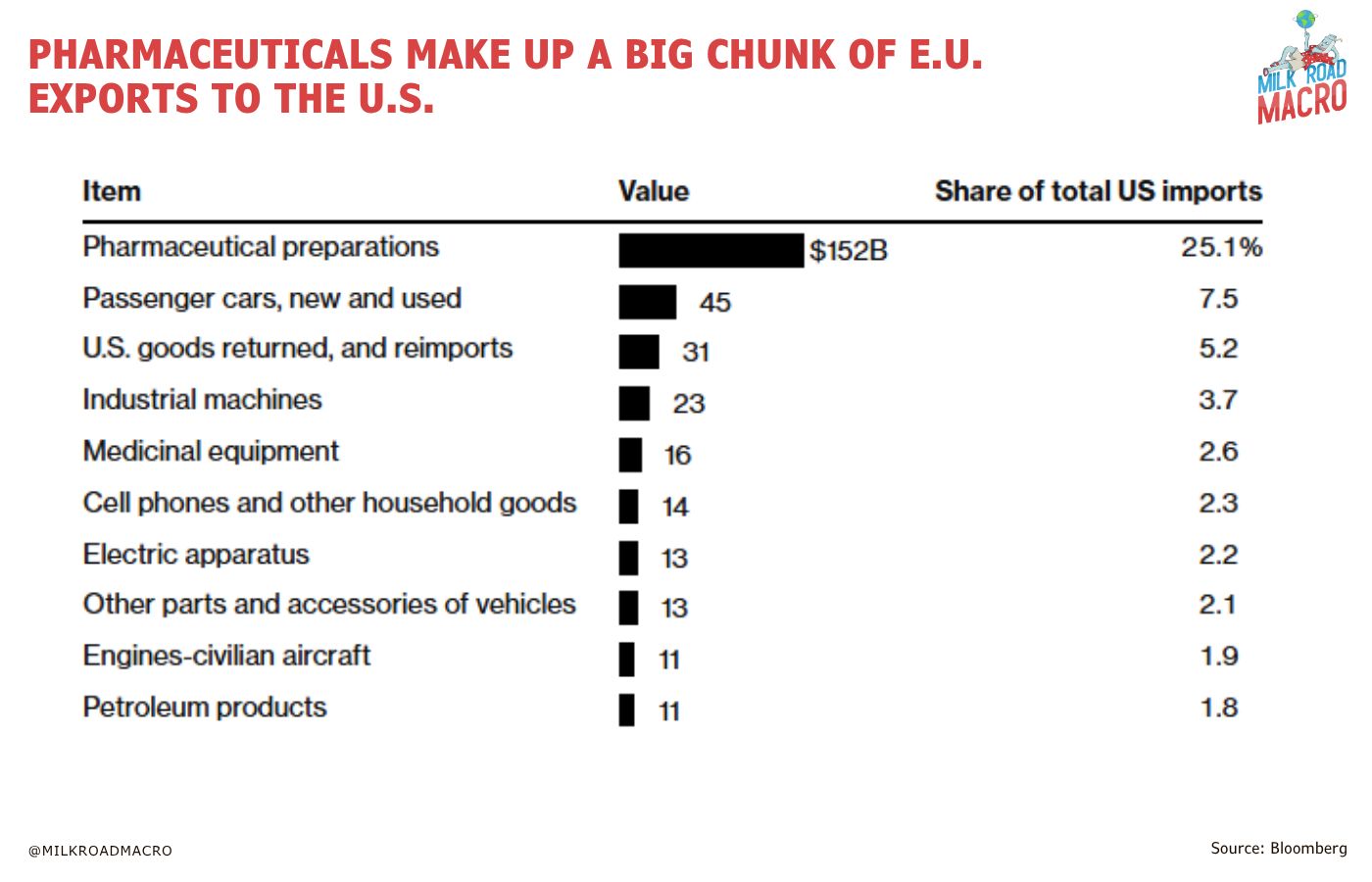

But this probably won’t include cars, steel, aluminum and pharmaceuticals, which may be subject to higher tariff rates.

Pharmaceuticals are an important segment, representing 25% of all EU exports to the US.

American imports to European Union countries will also face lower barriers as part of the new deal.

Additionally, the EU has agreed to purchase $750 billion in American energy products and invest $600 billion in the US on top of existing expenditures, according to Trump.

“It’s the biggest of all the deals”, Trump said.

Economists largely agree that the deal is a good thing.

An all-out trade war between the US and EU would have been the worst-case scenario, so the agreement brings a sense of relief to both sides.

But the new deal leaves EU exports facing much higher tariffs than the bloc charges for imports from the US.

An EU ambassador told the Financial Times there is no hiding the fact that the EU was “rolled over by the Trump juggernaut”.

They said: “Trump worked out exactly where our pain threshold is”.

Stephen Olson, a former US trade negotiator said: “The EU played a bad hand about as well as it could have”.

French Prime Minister Francois Bayrou said it was “a dark day” for the EU, and added that the EU had “resigned itself into submission”.

German Chancellor Friedrich Merz said the agreement would cause “considerable damage” to both Europe and the US and increase inflationary pressures.

So, just to recap, the US has now signed some kind of trade deal with the EU, Japan, the UK, Vietnam, Indonesia and the Philippines.

But an August 1 trade talk deadline still hangs over most other countries.

And what about China?

One of the most important countries to watch is China.

There is currently a separate August 12 deadline for Chinese trade talks.

But Chinese Vice Premier He Lifeng and US Treasury Secretary Scott Bessent are meeting in Stockholm this week for talks.

It’s likely that another extension will be made to the deadline, according to various reports.

At the heart of the haggling between the world’s largest economies is Beijing’s stranglehold on rare-earth magnets used to make everything from electric vehicles to high-tech weapons, and Washington’s curbs on cutting-edge chips essential to AI.

The US needs rare earths, and China needs AI chips - both have defence and security implications.

The Financial Times reports that the US Bureau of Industry and Security, which runs export controls, has been told to avoid tough moves on China, according to current and former US officials.

In April, the Trump team told Nvidia it would block the export of its H20 chip, designed for the Chinese market - but Trump has since reversed course.

Looking deeper into tariff effects

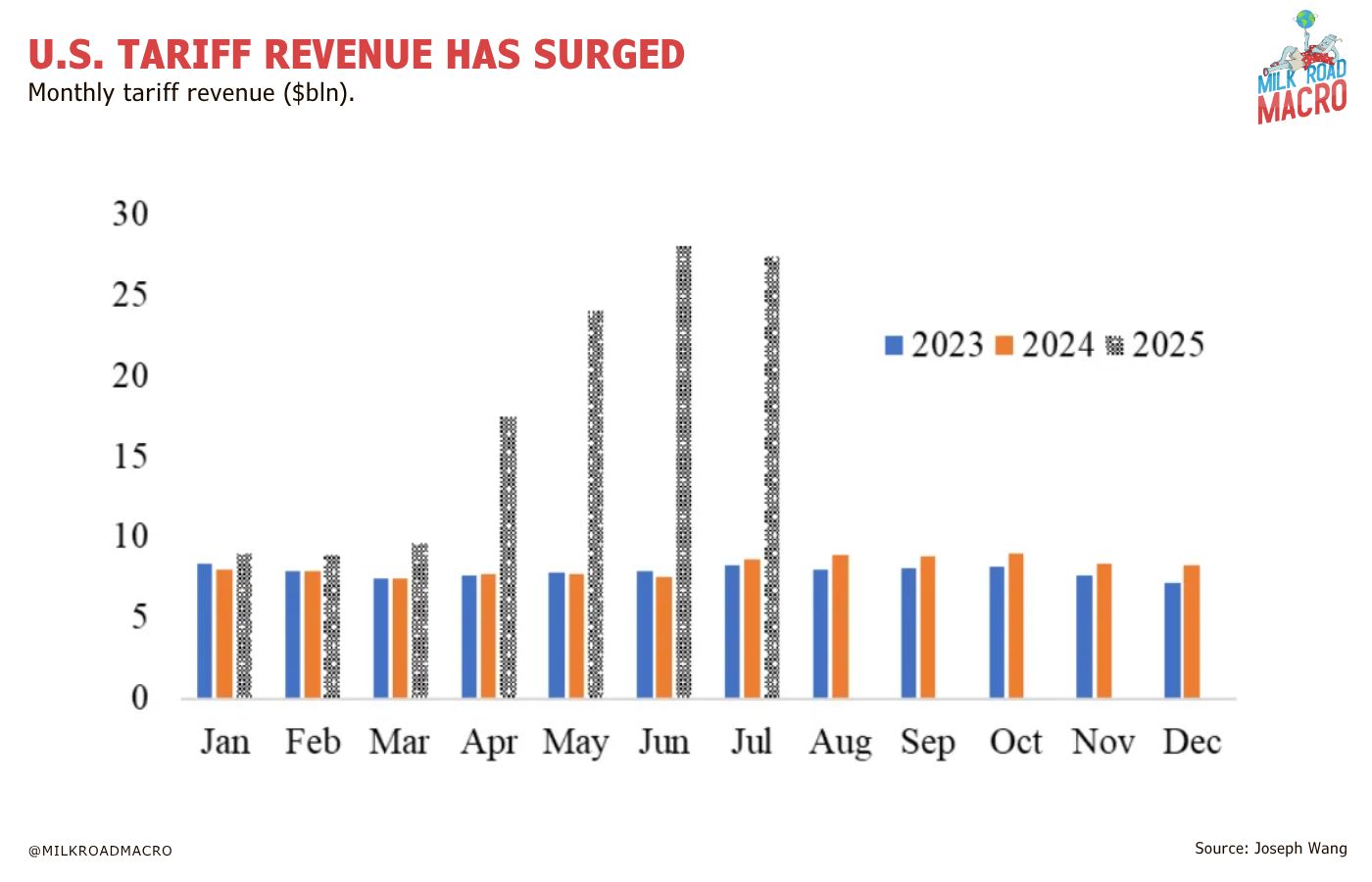

We are now seeing a meaningful surge in US tariff revenues as the levies start to stack up.

Tariff revenue has risen from about $8bn a month last year to around $25bn during the first three weeks of July.

Commerce Secretary Howard Lutnick has previously suggested that annual revenues could be as high as $700bn.

The tariffs need to be paid by somebody - whether it’s the exporter, the importer or the end consumer - somebody has to pay.

And we’re seeing a mixed picture in terms of who is fronting the bill.

In one instance, Japanese automakers absorbed the entire tariff, while in another case a US carmaker absorbed the tariffs on imported parts.

So, what does it all mean for markets?

After the EU deal was announced, both S&P 500 and Euro Stoxx (large cap European equities) futures initially bumped higher when trading began on Sunday evening.

Above all else, markets like certainty.

And the euro has also weakened significantly against the dollar.

I mentioned last week that positioning in the dollar is heavily bearish, and “short dollar” is now the most crowded trade in the world.

Price action this week may be another sign that the dollar (DXY) might be due for a period of upward correction/consolidation before any potential further downside.

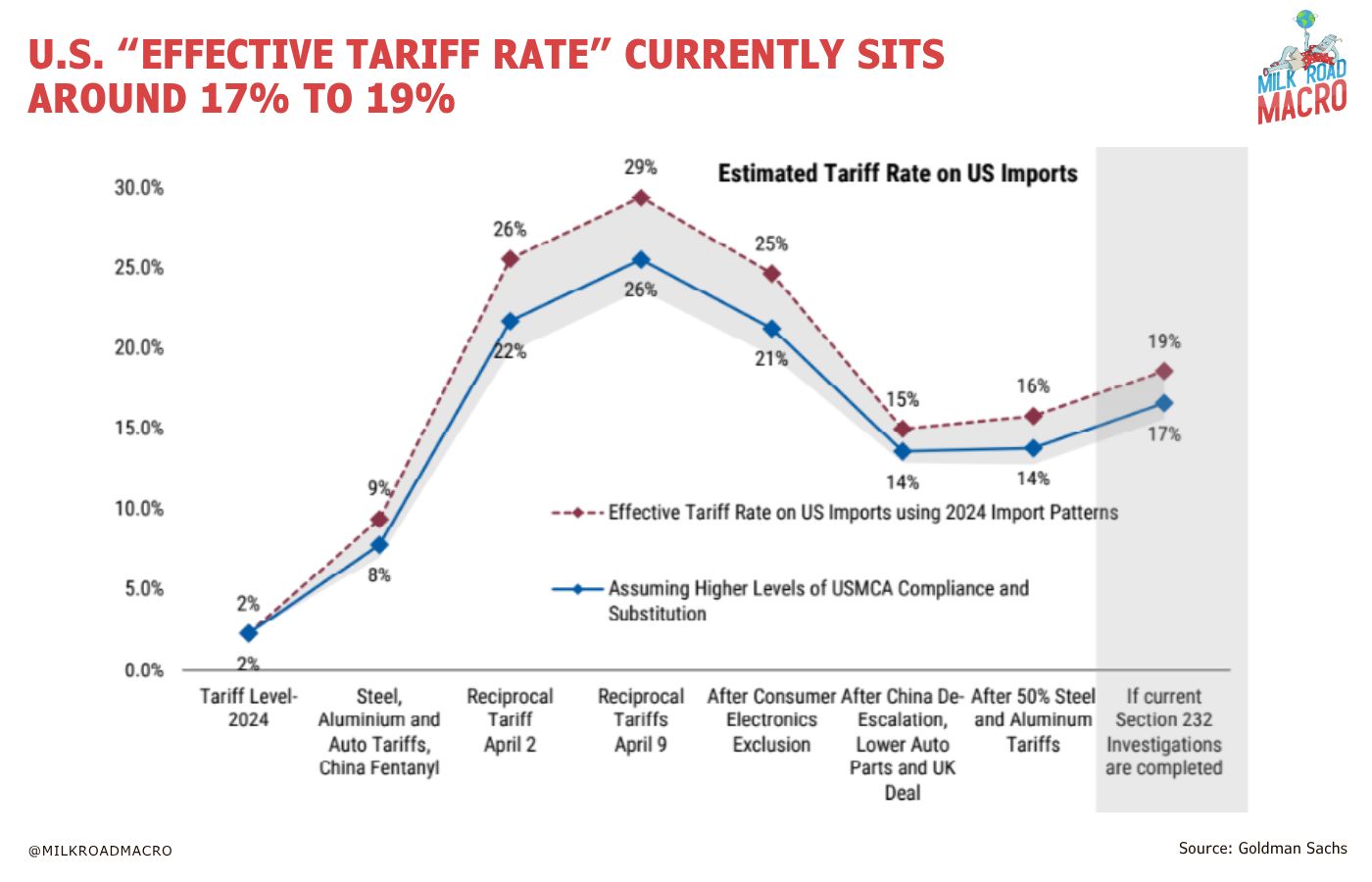

In a note to clients, Goldman Sachs Global Head of Fixed Income Michael Zezas outlined that the baseline “effective tariff rate” for the US is currently sitting around 17% to 19%, down from 26% to 29% in early April.

Judging by the overall market reaction so far, markets appear to be content with this expected tariff level.

But Zezas warned clients to be wary of overoptimism regarding tariffs, writing:

“We still believe the most likely outcome is slow growth and firm inflation.”

“Not a recession, but a backdrop where the adverse effects of trade on growth outweigh the boost from deregulation and fiscal largesse.”

“We see outcomes for the US economy skewing toward a slowdown, but with more clarity on the fiscal situation and deficits now front-loaded, the risk of a recession is easing.”

However, Zezas believes US stock indices will be able to ride out any potential short-term growth storm, writing:

“Our US equity strategy team posits (assumes) that slower growth won't interrupt the S&P's rally, crediting such tailwinds as earnings growth driven by a weaker dollar.”

Wrapping up

The tariff fog appears to be slowly lifting, with news of new deals trickling in.

There’s no doubt that the EU was a big one - and this will provide clarity for markets.

The next big one will be China - but it looks like it might be some time before something concrete occurs on this front.

Markets appear to be content with how tariffs are shaping up - so far.

But there is a potential risk of a hit to US growth in the short-term - although markets may be able to “see through” this potential growth hiccup.

Longer-term, tariffs may be beneficial to US growth and employment as businesses are incentivized to build in America, but those effects will take time to emerge.

That’s it for this edition - catch you for the next one.

INTRODUCING THE MILK ROAD MACRO PODCAST 🎙️

Yesterday, we were joined by PDS (the former head of Macro at George Soros) who broke down what he’s watching ahead of the FOMC meeting, how the AI revolution is affecting the economy, and how he’s reading the macro environment right now.

You can listen right now over on the freshly launched Milk Road Macro YouTube channel.

Tomorrow, we go live with Tony Greer right after Powell speaks.

Will rates get cut? Will Powell drop a bombshell?

Either way, we’ll be breaking it all down.

But wait, there’s more!

Want a free year of Macro PRO when it launches this August?

Here’s how to enter:

Subscribe to the Milk Road Macro YouTube channel

Screenshot the proof

Post it on X and tag @MilkRoadMacro before midnight Thursday

We’ll be picking a random winner this Friday. The prize is one full year of Macro PRO completely free, including direct access to John and Tomas inside the Macro PRO Discord community, one live AMA per month, and two Macro PRO reports.

It’s the kind of thing funds pay thousands for, and you might get it for free.

The Dallas Federal Reserve reported a big pick-up in factory activity in July, as its production index rose to the highest level for more than three years. We previously outlined why a number of indicators are pointing to an upturn in the business cycle ahead (bullish).

The Federal Reserve’s FOMC meeting begins today - with a rate decision and a Jerome Powell press conference tomorrow. Markets are expecting no change in rates, but attention turns to if Powell will provide any forward guidance for the rest of the year.

Commerce Secretary Howard Lutnick said a 90-day extension of a trade truce with China was a likely outcome. “It seems that way, but let’s leave it to President Trump to decide”, Lutnick said.

RATE TODAY’S EDITION

What'd you think of today's edition? |

MILKY MEME 🤣

ROADIE REVIEW OF THE DAY 🥛